BlockChain Facts: Meaning of Blockchain, How it can be used and how it Works

ou might be familiar with spreadsheets or databases. A blockchain is somewhat similar because it is a database where information is entered and stored. The key difference between a traditional database or spreadsheet and a blockchain is how the data is structured and accessed.

What Is a Blockchain?

Blockchain is a decentralized digital ledger that securely stores records across a network of computers in a way that is transparent, immutable, and resistant to tampering. Each "block" contains data, and blocks are linked in a chronological "chain."

A blockchain is a distributed database or ledger shared across a computer network's nodes. They are best known for their crucial role in cryptocurrency systems, maintaining a secure and decentralized record of transactions, but they are not limited to cryptocurrency uses. Blockchains can be used to make data in any industry immutable—meaning it cannot be altered.

Since Bitcoin's introduction in 2009, blockchain uses have exploded via the creation of various cryptocurrencies, decentralized finance (DeFi) applications, non-fungible tokens (NFTs), and smart contracts.

Key Takeaways

- Blockchain is a type of shared database that differs from a typical database in the way it stores information; blockchains store data in blocks linked together via cryptography.

- Different types of information can be stored on a blockchain, but the most common use has been as a transaction ledger.

- In Bitcoin’s case, the blockchain is decentralized, so no single person or group has control—instead, all users collectively retain control.

- Decentralized blockchains are immutable, which means that the data entered is irreversible. For Bitcoin, transactions are permanently recorded and viewable to anyone.

How Does a Blockchain Work?

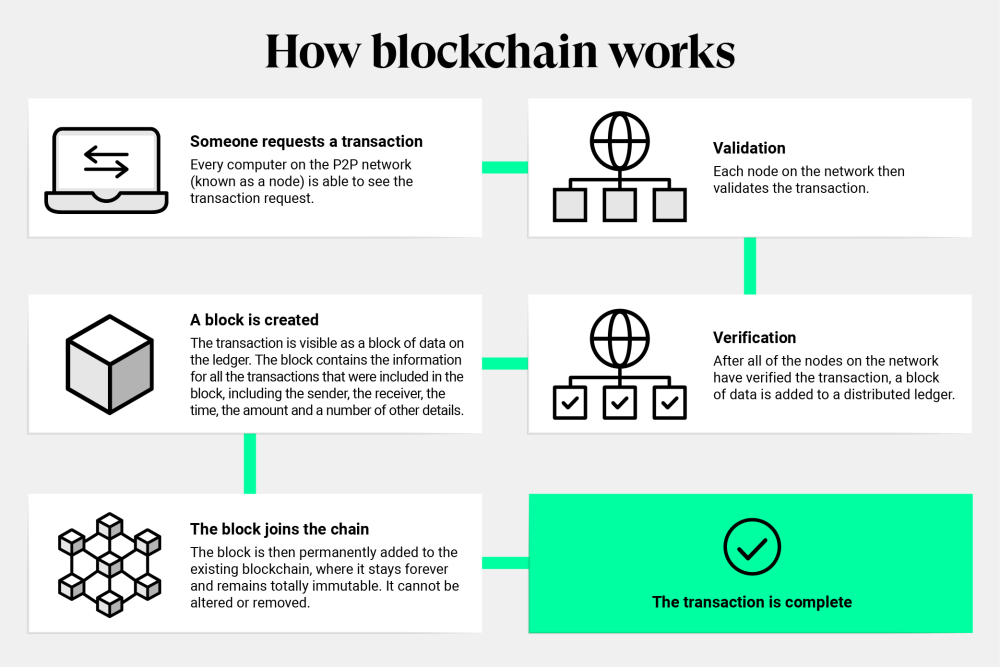

A blockchain consists of programs called scripts that conduct the tasks you usually would in a database: entering and accessing information, and saving and storing it somewhere. A blockchain is distributed, which means multiple copies are saved on many machines, and they must all match for it to be valid.

The Bitcoin blockchain collects transaction information and enters it into a 4MB file called a block (different blockchains have different size blocks). Once the block is full, the block data is run through a cryptographic hash function, which creates a hexadecimal number called the block header hash.

The hash is then entered into the following block header and encrypted with the other information in that block's header, creating a chain of blocks, hence the name “blockchain.”

Every node in the network proposes its own blocks in this way because they all choose different transactions. Each works on their own blocks, trying to find a solution to the difficulty target, using the "nonce," short for number used once.

The nonce value is a field in the block header that is changeable, and its value incrementally increases with every mining attempt. If the resulting hash isn't equal to or less than the target hash, a value of one is added to the nonce, a new hash is generated, and so on. The nonce rolls over about every 4.5 billion attempts (which takes less than one second) and uses another value called the extra nonce as an additional counter. This continues until a miner generates a valid hash, winning the race and receiving the reward.

What Is Decentralization in Blockchain?

Decentralization is at the core of blockchain technology, distributing control across multiple participants instead of a central authority. This shift ensures greater security, transparency, and autonomy for users. Learn how decentralized networks work, their key benefits, and the challenges they face in creating a more open and fair digital world.

Decentralization within blockchain means the even distribution of control across multiple operators through what we call nodes. Nodes are single devices that participate in the blockchain by running its software and storing a copy of the network.

Power is distributed across all these nodes to make sure that no single entity can gain control of the system and tamper with it.

Whenever a decision must be made, every node has to validate and approve it unanimously. This process is known as consensus, and it makes the blockchain more transparent and secure.

As you can see, the process is different from a centralized system with a single authority where only one person makes the whole decision. Single authority systems are prone to manipulation and censorship—things you won’t find in blockchains thanks to decentralization.

How Decentralization Works in Blockchain

I mentioned that decentralization works on a consensus basis through the nodes. But that’s just one of the different ways decentralized technology works. Plus, consensus algorithms go beyond just that simple explanation.

Let’s break down the three top mechanisms blockchains use to achieve decentralization:

- distributed ledger technology (DLT)

- consensus algorithms

- peer-to-peer networks

Distributed ledger technology is powered by nodes, where every participant maintains a copy of the entire transaction history in the network.

Consensus algorithms include protocols like Proof of Work, Proof of Stake, and Proof of Staked Authority. These protocols enable network participants to agree on the state of the blockchain—no need for a central authority.

In peer-to-peer networks, every network participant can transact with each other directly. For instance, you can send Bitcoin directly to someone else without having to go through a middleman. Transactions are faster since no intermediary or central authority manages them on your behalf.

All three mechanisms work together to make blockchains decentralized.

Challenges of Decentralization

Of course, such an innovative idea wouldn’t be truly invincible. Decentralization also has its challenges, and we’ll cover each one, including scalability, governance, and even managing the entire network.

When it comes to scalability, decentralized networks often face a lot of challenges. The most crucial challenge is processing large numbers of transactions quickly and efficiently. This scalability problem can lead to slower transaction times and higher fees during periods of high network activity. The problem also limits the widespread adoption of blockchain technology.

Governing a decentralized network is also a big, complex issue that takes up lots of time compared to centralized systems. The lack of a central authority means that reaching consensus among network participants on important updates or protocol changes can be a lengthy and sometimes contentious process.

The distributed nature of decentralized systems can make them more challenging to manage and maintain compared to centralized alternatives. This complexity often requires users to have a deeper understanding of the technology, which can create a barrier to entry for less tech-savvy individuals and potentially slow down mainstream adoption.

Chiliz Chain has the largest mainstream sports partner network in blockchain, and a massive potential mainstream audience. We see it as our responsibility to provide educational materials that relate to the entire sector, increasing security, understanding and adoption of this incredible technology.

Bitcoin vs. Blockchain

Blockchain technology was first outlined in 1991 by Stuart Haber and W. Scott Stornetta, two researchers who wanted to implement a system where document timestamps could not be tampered with.4 But it wasn’t until almost two decades later, with the launch of Bitcoin in January 2009, that blockchain had its first real-world application.

Bitcoin

The Bitcoin protocol is built on a blockchain. In a research paper introducing the digital currency, Bitcoin’s pseudonymous creator, Satoshi Nakamoto, referred to it as “a new electronic cash system that’s fully peer-to-peer, with no trusted third party.”5

The key thing to understand is that Bitcoin uses blockchain as a means to transparently record a ledger of payments or other transactions between parties.

Blockchain

Blockchain can be used to immutably record any number of data points. The data can be transactions, votes in an election, product inventories, state identifications, deeds to homes, and much more.

Currently, tens of thousands of projects are looking to implement blockchains in various ways to help society other than just recording transactions—for example, as a way to vote securely in democratic elections.

The nature of blockchain's immutability means that fraudulent voting would become far more difficult. For example, a voting system could work such that each country's citizens would be issued a single cryptocurrency or token.

Each candidate could then be given a specific wallet address, and the voters would send their token or crypto to the address of whichever candidate they wish to vote for. The transparent and traceable nature of blockchain would eliminate the need for human vote counting and the ability of bad actors to tamper with physical ballots.

How Are Blockchains Used?

As we now know, blocks on Bitcoin’s blockchain store transactional data. Today, tens of thousands of other cryptocurrencies run on a blockchain. But it turns out that blockchain can be a reliable way to store other types of data as well.

Some companies experimenting with blockchain include Walmart, Pfizer, AIG, Siemens, and Unilever, among others. For example, IBM has created its Food Trust blockchain to trace the journey that food products take to get to their locations.6

Why do this? The food industry has seen countless outbreaks of E. coli, salmonella, and listeria; in some cases, hazardous materials were accidentally introduced to foods. In the past, it has taken weeks to find the source of these outbreaks or the cause of sickness from what people are eating.

Using blockchain allows brands to track a food product’s route from its origin, through each stop it makes, to delivery. Not only that, but these companies can also now see everything else it may have come in contact with, allowing the identification of the problem to occur far sooner—potentially saving lives. This is one example of blockchain in practice, but many other forms of blockchain implementation exist or are being experimented with.

Blockchain security

Blockchain is frequently claimed to be an “unhackable” technology. But 51% attacks allow threat actors to “gain control over more than half of a blockchain’s compute power and corrupt the integrity of the shared ledger. … While this particular attack is expensive and difficult, the fact that it was effective means that security professionals should treat blockchain as a useful technology—not a magical answer to all problems.”

The 51% attack takes advantage of what is known as the 51% problem: “If a single party possesses 51% of a mining pool, it is possible to falsify an entry into the blockchain, allowing for double spending, and even to fork a new chain to the advantage of the mining pool.”

The two main types of blockchain, public and private, offer different levels of security. Public blockchains “use computers connected to the public internet to validate transactions and bundle them into blocks to add to the ledger. … Private blockchains, on the other hand, typically only permit known organizations to join.” Because any organization can join public blockchains, they might not be right for enterprises concerned about the confidentiality of the information moving through the network.

Another difference between public and private blockchains regards participant identity. Public blockchains “are typically designed around the principle of anonymity. … A private blockchain consists of a permissioned network in which consensus can be achieved through a process called ‘selective endorsement,’ where known users verify the transactions. The advantage of this for businesses is that only participants with the appropriate access and permissions can maintain the transaction ledger. There are still a few issues with this method, including threats from insiders, but many of them can be solved with a highly secure infrastructure.”

Blockchain technologies are growing at an unprecedented rate and powering new concepts for everything from shared storage to social networks. From a security perspective, we are breaking new ground. As developers create blockchain applications, they should give precedent to securing their blockchain applications and services. Activities such as performing risk assessments, creating threat models, and doing code analysis, such as static code analysis, interactive application security testing, and software composition analysis, should all be on a developer’s blockchain application roadmap. Building security in from the start is critical to ensuring a successful and secure blockchain application.

What's Your Reaction?

Like

5

Like

5

Dislike

0

Dislike

0

Love

1

Love

1

Funny

0

Funny

0

Angry

1

Angry

1

Sad

0

Sad

0

Wow

0

Wow

0

-

NSENGUMUREMYI Jean BaptisteGreat news BTC RISES AS EQUITY MARKETS SWOON

NSENGUMUREMYI Jean BaptisteGreat news BTC RISES AS EQUITY MARKETS SWOON -

JunoGreat lecture